To get the best lending results, compare all P2P lending and IFISA providers that have gone through 4thWay’s rigorous assessments.

RateSetter Review – Investment Analysis By 4thWay

4thWay's RateSetter Review

4thWay's RateSetter Review

RateSetter is sold to Metro Bank and repays all lenders with a profit

RateSetter itself was sold to Metro Bank in 2020 and was no longer available to new lending. In early 2021, RateSetter's P2P loans were sold to Metro Bank.

All lenders in RateSetter made a profit on their lending since it started in 2010.

RateSetter lenders easily beat inflation over more than 10 years of lending. Although during the pandemic some lenders might have rougly broken even with inflation, they will still have earned considerably more than the average saver with a savings account.

We wrote about RateSetter's sale to Metro Bank in terms of the sale price in What Investors Can Learn From RateSetter's Sale To Metro Bank. If and when we get more details on the sale of the remaining P2P loans to Metro Bank, we'll add a few notes on it here.

Here is our final review of RateSetter before it closed to new lending.

This RateSetter review, written by one of the world's foremost authorities on peer-to-peer lending, is in two parts. The first part is taken our Quick Expert Review series, which quickly covers the author's main points and opinions.

The second part makes up the rest of the full RateSetter review, which is especially for people who require a lot more information before making decisions with their money.

My RateSetter Review in one sentence

RateSetter will beat savings accounts and cash ISAs most of the time for decades to come.

[orangebox title=”RateSetter Review Main Points – 8 Minute Read”]What does RateSetter do?

RateSetter offers peer-to-peer investors and IFISA investors a blend of different types of lending.

It mostly does UK personal lending to creditworthy people, repaid within five years. These include a mix of both standard loans as well as many smaller loans to cover mobile-phone purchases.

RateSetter lending is also to property developers, which makes up [RateSetterPropertyLendingFraction] of its recent loans.

A small amount is lending to businesses, often to help car dealerships purchase stock. It has greatly reduced the amount of small business lending it does, since one of my colleagues wrote the previous RateSetter review.

This mix of different types of lending is not just a curiosity. At times, it could reduce risks for lenders. It would do this by making the outstanding basket of loans more stable through different economic situations.

RateSetter offers lending interest rates of up to 2.0%, protected by a reserve fund to cover expected bad debts.

When did RateSetter start?

RateSetter started in 2010 and it's now completed £4.1 billion.

What interesting or unique points does RateSetter have?

The most startling feature RateSetter has is that it spreads all lenders' risk across all its outstanding loans, which number in the hundreds of thousands. I can't emphasise enough how valuable that is. It means there's no risk that you'll lose money through pure bad luck.

That paragraph is worth reading twice, because it's easy to overlook the importance – and power – of spreading your money around.

Lenders are also protected by a large reserve fund, which RateSetter calls the Provision Fund. It's worth £25 million and includes amounts due to be paid in from existing borrowers. It's the equivalent of 5.5% of RateSetter's outstanding loan book and it's more than the forecast future bad debts. It's gained size to keep pace with the changing mix of loans, so its future looks bright and solid.

As a result of the reserve fund, none of RateSetter's current 87,000 lenders, nor its past lenders, have lost a penny. And all have earned every penny of interest that they expected to.

So far, it has a record of allowing lenders to exit early in an average time of one day. This means lenders who need their money back have rapidly sold their loans to other lenders. As with all peer-to-peer lending platforms, there will be times when lenders have to wait for a sale or for borrowers to repay their loans naturally. But RateSetter's record is excellent.

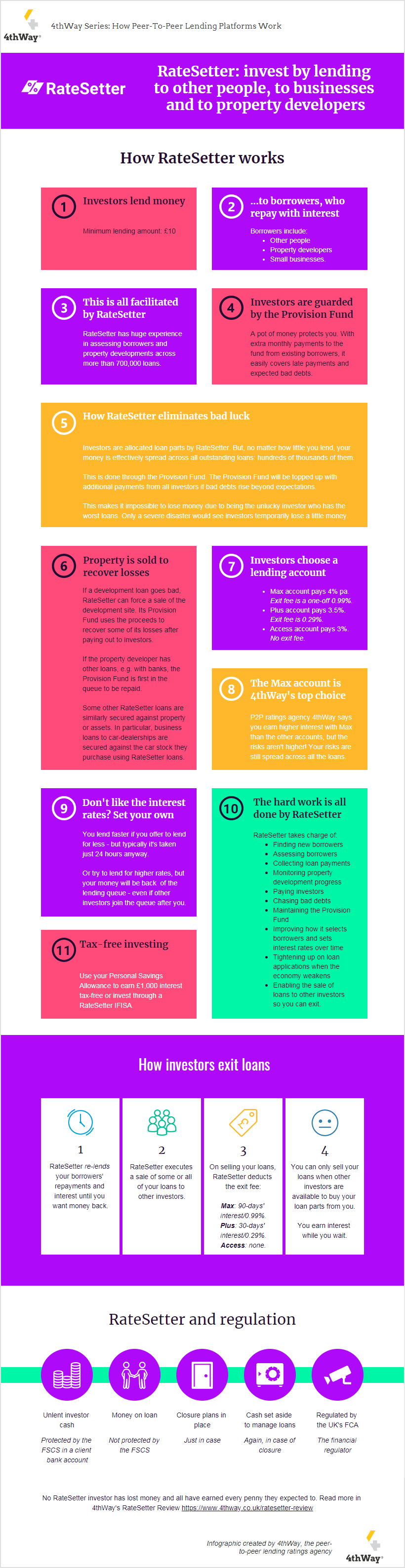

RateSetter review: how does RateSetter work?

Pictures speak louder than words:

4thWay's RateSetter review infographic: click to expand to see How does RateSetter work?

RateSetter during COVID-19

Existing lenders are still receiving positive interest at this stage and we have seen no reason why RateSetter will not do well for existing lenders. Not even the pandemic and the extraordinary lockdown that followed. Even if any existing lenders do ever move into an overall loss, it will take little time to earn enough interest to recover those losses.

New lending is a different story. RateSetter has temporarily halved interest rates on new lending in order to divert more money to its reserve fund. Lending interest rates now are simply not attractive enough compared to savings accounts or to the risks involved. Therefore, lenders should switch off re-lending, and new lenders should currently avoid RateSetter until it restores its interest rates.

You should know that the rest of this review has not been updated based on the impact of COVID-19. Our view of RateSetter is otherwise unchanged.

RateSetter review: how good are its loans?

RateSetter's standards are reassuring for all types of lending.

It accepts a wide range of personal borrowers, but every borrower needs to show that they can afford the loans. It mostly targets borrowers in the prime lending space. It throws in a good measure of borrowers from further up the risk scale. Yet RateSetter has an impressive record across many years showing that it sets borrower interest rates and payments to Provision Fund appropriately, based on the risk in each loan.

Recovery of bad debt is never a big feature in standard personal loans, because most of the outstanding debt is usually written off. It's more important to contain the number of loans that turn bad in the first place. Even so, it's reassuring that the bad debt outstanding has been sharply in line with 4thWay's models. Those are based on results from similar banks, showing a similar quality.

Its development loans are “typically” for no more than 65% of the hoped-for sale price of the completed development. Developers also need to stump up at least 20% of the development costs. Both of these are sensible and comparable to other development lenders.

RateSetter keeps it simple by ensuring that its lenders are always legally first in the queue. They will get their money back before anyone else if anything goes wrong, and the development site is forcibly sold.

RateSetter review: lending processes

This peer-to-peer lending platform has long demonstrated to 4thWay that its processes for lending are sophisticated. It competently conducts the credit, fraud and other checks that we would expect to see for the types of lending that it provides. It constantly measures its results and learns from its performance. It has a very deep set of loans – 850,000 of them. This enables it to learn how it can set borrower interest rates more accurately.

Bad debts and the RateSetter Provision Fund

With personal lending, unless a peer-to-peer lending site's processes are pretty wacky, it's not always possible to know whether it genuinely uses sensible standards or is talking a good game – until you see the actual results. Luckily, RateSetter has an impressively deep record showing it walks as well as it talks.

In recent years, four in every 100 personal loans that were outstanding during a given year have turned bad. Most of those loans were partly repaid before turning bad and some of them saw recoveries occur afterwards. This is somewhat more personal loans turning bad than we see at the banks 4thWay uses for benchmarking. But when combined with an enlarged reserve fund, the difference is sufficiently covered.

On its development loans, RateSetter's focus above all is on containing the risks – which is exactly what you need here. Such loans are higher risk in the wrong hands. But RateSetter has just one borrower that has had bad debts out of more than 400 development borrowers. Two-thirds of property developers having fully repaid all their loans and the rest are ongoing.

RateSetter pays a proportion of the proceeds of every loan into its Provision Fund. This is a pot of money held in reserve to cover expected bad debts, including unpaid interest. The more risky it perceives a borrower to be, the more it will pay into the Provision Fund for that loan. The amount paid in is set by its risk team. I am satisfied with the level paid in.

How good are RateSetter's interest rates?

Since our last RateSetter review, it has changed its lending accounts and lowered the lending interest rates.

RateSetter lenders are now paid 1.5% when lending in the Access account/Access IFISA. You're paid 1.75% for the Plus account/IFISA or 2.0% for the Max account/IFISA.

Here's another rather astounding point about RateSetter: it's a case where higher rates mean lower risk. Because its higher-rate accounts are lower risk than its lower-rate ones.

It works like this: your risks are spread across all RateSetter's loans. That's regardless of the account you lend in and the interest rate you're earning. The higher-paying Max account pays more interest and therefore pays you more cover against the risk of bad debts. That's assuming the reserve fund ever proves insufficient and needs to be topped up from interest earned by all lenders.

The RateSetter Max account therefore has the edge over the lower-paying accounts.

Does RateSetter offer a large margin of safety?

As a result of equal risks across all accounts but different interest rates, the top two paying accounts currently earn the highest 4thWay PLUS Rating of 3/3, “Exceptional”. The Access account has a 2/3, “Excellent” rating.

An Exceptional rating means we calculate the lending account will offer positive returns through a severe recession and property crash. By which I mean similar to 2008.

The Access Account, with its Excellent rating, will still offer positive returns through a moderate recession and property crash.

The 4thWay PLUS Ratings are calculated using all the individual loans in RateSetter's huge loan book. We use a stricter version of the international banking tests (Basel stress tests). As usual, we factor in other defences – called “credit enhancements” – such as RateSetter's reserve fund.

For the loans and protections that lenders are offered, I consider RateSetter's interest rates in the Max account to be highly satisfactory, offering a sufficiently large margin of safety. The other accounts also offer a satisfactory margin, although lenders need to watch out for any further reductions.

How much experience do RateSetter's key people have?

Usually when I write about the experience of people at a peer-to-peer lending website it usually goes two ways. Either there's one highly experienced person to write about, or there's much to say about large gaps in skills.

But RateSetter has a huge and experienced team. They cover all the skills we'd expect to see at any serious banking operation. From the key decision maker in the credit-risk team, and on to the other required areas. This means property loan originations, personal and business loan underwriters, bankers and data analysts, and bad-debt recovery. I can see no shortfall in any areas.

Has RateSetter provided enough information to assess the risks?

RateSetter regularly provides 4thWay with very detailed information about all the loans it's ever approved, and how those loans have performed. Since it has now completed 850,000 loans, this provides us with a huge history to assess its ability and the inherent risks.

Of the “big three” peer-to-peer lending platforms, RateSetter is by far the most open with 4thWay. It responds to our probing. It provides a huge amount of background information that enables us to better understand its processes and standards. And it regularly gives us a vast trove data about every one of its loans.

RateSetter has shared more information with us about how it selects borrowers and sets interest rates than its biggest competitors. It makes its key people available to us for meetings and interviews.

We have sufficient information to assess the risks.

Is RateSetter profitable?

RateSetter has matured in a sustainable way. It grew revenue (the money it makes from sales) rapidly for eight years. Its earnings have been stable at around £33 million for each of the past two years.

Now, attention turns to its bottom line: profits.

Like most peer-to-peer lending websites, RateSetter still isn't profitable. However, its losses narrowed from £27 million last year to £4 million. Over the past year, its assets grew at roughly the same pace as its debts. As a deeply entrenched player in the loan and P2P space, I firmly believe that RateSetter will become profitable.

Is RateSetter a good investment?

RateSetter is run with discipline. I consider it likely that it will offer stable, satisfactory returns, beating savings accounts and cash ISAs, the vast majority of the time, for many decades to come. I consider RateSetter a good investment.

What is RateSetter's minimum lending amount and how many loans can I lend in?

RateSetter minimum investment is just £10. One problem with many other peer-to-peer lending platforms is that you can't easily spread your money across lots of loans. But with RateSetter, even when you put in its minimum amount, the risks are spread across hundreds of thousands of loans. This is far more diversification than you actually need.

Does RateSetter have an IFISA?

RateSetter's lending accounts are all available as IFISAs.

What more do I need to know?

I just wonder if RateSetter makes it clear enough to lenders that they might sometimes suffer severe exit delays. RateSetter can't guarantee that you will be able to sell your loans to someone else before your borrowers repay them. Delays might occur in particular when the economy or interest rates change rapidly. While you continue to earn interest on those loans until they're fully repaid, all P2P websites have that same risk.

RateSetter Review: their best-rated product

This account is currently paying 2.0% interest.

Read about the 4thWay PLUS Ratings, compare more peer-to-peer lending accounts or visit RateSetter.

RateSetter is running a cashback offer of £100 for lending at least £1,000. Read more in P2P Lending And IFISA Cashback Deals Available Now.

[/orangebox]Full RateSetter Review: what's new at RateSetter?

New since our previous RateSetter Review, the biggest change so far in 2019 is its new lending accounts:

RateSetter's new lending accounts

RateSetter has scrapped its three previous accounts and replaced them with Max, Plus and Access.

The older accounts were based on how long you wanted to lend for. So, if you used the one-year lending account, you were typically allocated loans that lasted one year or less.

Now, lenders are not allocated loans of any specific length. Instead, you might be allocated any loans lasting from a few months to five years.

This enables a new system with one pool of loans shared by all lenders, regardless of the account you lend in. Having just one, larger pool of loans makes it easier for RateSetter to manage the flow of money as lenders want to start or stop lending.

Re-lending borrower payments is now compulsory

With these new accounts, it's no longer possible to choose to leave naturally by allowing your borrowers to simply repay you gradually.

Now, RateSetter will always re-lend the money and interest you receive from a borrower until you choose to leave.

That said, if there are no lenders available to buy your loan parts off you, it will stop re-lending your money. Then, until it's able to sell your loan parts for you, it will allow natural repayments to you to steadily release your money. You continue to earn interest while money is being lent.

Why use RateSetter?

Lending through RateSetter is one of the easiest ways to spread your money around very quickly. Your money is not just spread across lots of loans, but different types of loans. It will never be the most exciting investment, but it's suitable for anyone building a balanced or low-risk peer-to-peer lending portfolio.

RateSetter review: exit costs

Aside from interest rates, the main difference between the three lending accounts are the exit costs:

- RateSetter Access has no fee for selling up.

- RateSetter Plus costs you 30-days' interest.

- RateSetter Max costs you 90-days' interest.

The exit cost is charged at the currently advertised lending rate – which RateSetter calls the Going Rate. For example, if the going rate is 4% and the charge is 90-days' interest, the exit cost to you is 0.99%. (That's 4% divided by 365 times 90.)

You need to lend for at least three months to earn enough interest to cover the cost of leaving in the Max account and at least one month for the Plus account.

If interest rates fall after you start lending then the exit cost will be lower. If they rise when you start lending, they will be higher. This will increase or decrease the length of time you need to lend to cover the exit costs.

Remember that, just because Access is free to leave, it doesn't mean it's easier to leave.

How long should I lend for at RateSetter?

You need to lend long enough to cover any exit costs. This will usually be no longer than three months.

You should be prepared to lend at least a portion of your money for many months longer than you expected. That's in case you're unable to sell as quickly as usual.

Typically in peer-to-peer lending, you need to assume that you'll be lending for several years, in case your loans get off to a bad start and you need a bit of time to recover and end up with positive returns.

This will rarely be the case at RateSetter, due to its protections for lenders. With each month you earn interest, the risk of making an overall loss rapidly shrinks.

While I can't rule out some unfortunate lenders having very bad timing when a substantial recession comes, I don't believe lenders should generally expect to have to lend for years in order to get satisfactory returns.

How much should I lend at RateSetter?

Since your risks are effectively spread across all loans by means of the Provision Fund, you don't have to lend more than £10 to lend sensibly.

Judging the upper amount that might be prudent to lend requires, in particular, an understanding of the key risk: the risk of bad debts.

At the end of 2019, RateSetter's lending accounts have a very good 4thWay Risk Score of 4/10 on all its lending accounts. The lower, the better.

4thWay Risk Scores ignore interest earned and focus on bad debts. A 4/10 4thWay Risk Score means that we forecast average losses after reserve fund payouts but before interest of 2.5%-5% over the full life of the loans, during a severe recession.

Those losses are one-off, whereas interest earned on the loans usually lasts years. That makes it easier to offset losses. It doesn't take much interest earned over a year or two to offset those losses.

Few peer-to-peer lending websites and IFISA providers have scored better than this. And none spread your money across so many, varied loans.

I think lenders can sensibly lend more through RateSetter than most of its competitors. A limit of 30% of the total pot of money available for investing is a reasonable limit. If you're new to peer-to-peer lending, you're restricted to just 10% in the first year, so that you have time to familiarise yourself with it.

I still recommend you lend across at least six different peer-to-peer lending sites, if you're putting a lot of your money into this type of investment. But you can lend smaller amounts through other peer-to-peer lending and IFISA providers.

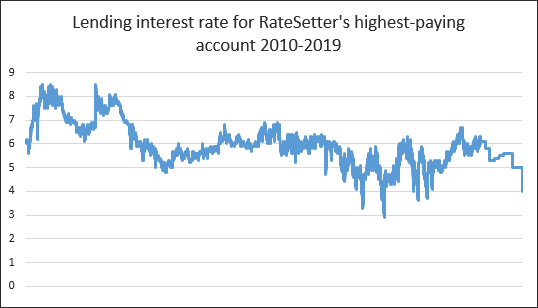

What returns have lenders had in the past?

Lenders have received every penny of interest they expected to in the near-10 years RateSetter has been around. For those who chose to lend in the highest-rate account, they have earned an average 5.96%. That's since RateSetter started in 2010 until 21st November 2019.

The lion's share of interest and fees paid by borrowers has either been paid to lenders in interest or gone into RateSetter's Provision Fund to cover bad debts on lenders' behalf.

Interest rates have fallen – as expected

You can see from the graph below that lenders earned more in the earlier years and now earn 2.0%.

RateSetter lending rates are not the lowest they've ever been, but they've generally trended downwards since RateSetter began. Since the launch of the new lending accounts, rates have dropped twice: by around 1.5 percentage points in the highest-paying account.

This pattern is normal in peer-to-peer lending, for reasons covered by Matt Howard in Why Do Peer-To-Peer Lending Rates Fall? 5 Reasons.

The fall in rates is in line with 4thWay's expectations for a lending platform that is reaching maturity. It doesn't weaken the case for investing in RateSetter.

However, the space for rates to fall further is shrinking and so this is something to watch.

RateSetter review 2019: how variable are lenders' results?

Lending through RateSetter is predictable. Lenders who lend at the going rate (the advertised lending rate) and who use the same lending account have had almost identical results.

The slight historical differences only exist at all because, until recently, the rates fluctuated just a little every day. So the time or day lenders lent their money might sometimes have added or shaved off a fraction of one percent.

Now, even this small variation has been eliminated. Lenders using the going rates earn exactly the same.

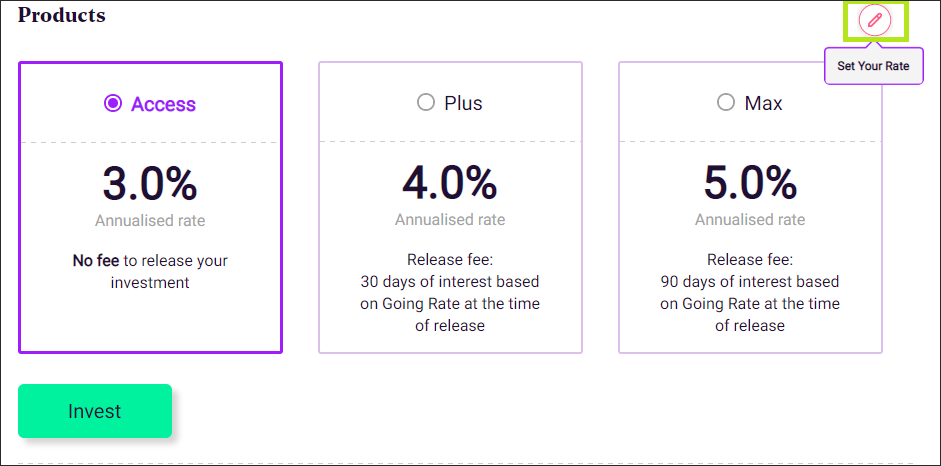

Choosing your own lending rate

Most money lent through RateSetter is lent at the going rate. But you can request to lend at a lower or higher rate. RateSetter knows this feature doesn't interest everyone. That's why it's easy to miss the button to “Set your rate” when you choose your lending account:

If you choose to lend at a lower rate, you'll get your money lent out faster than those lending at the going rate in any of RateSetter's lending accounts. Consider this step if lending slows to take longer than a week, rather than just one day.

Some RateSetter lenders attempt to make more money by setting a higher rate. The downside is that anyone looking to lend at the going rate will be prioritised ahead of you. That's even if they join the lending queue after you.

At any one time, there can be several million pounds queued for lending at the going rate and several million queued at a higher rate.

We have no data about how many people have successfully lent money at the higher rate or how long it has taken them to get their money lent.

Are future bad debts well covered by the Provision Fund?

Bad debts on personal lending

Bad debts on RateSetter's personal loans have been steady for quite a few years and all the signs buried within the loan book currently point to no change. This demonstrates that RateSetter has a strong understanding of its individual borrowers.

Bad debts on business lending

RateSetter's business loans are larger in size than its personal loans. But they now make up a relatively small proportion of RateSetter's overall lending.

In 2018, RateSetter approved just 500 small business loans. In both 2016 and 2017, it approved three times as many. 2019 is concluding with even fewer business loans.

The impact of business lending on RateSetter's results in future is small and getting smaller. This lowers the proportion of loans that turn bad, since small business lending suffered the highest proportion of loans that went into default.

Development loans

RateSetter's record on development loans has been superb so far. The uniformity of its success in this space shows that its bad debts will remain attractively low compared to competitors.

Future bad debts on all loans

Forecasting is an art rather than a science, and it's difficult at the best of times. With the variety of loans RateSetter does, it's particularly tricky.

Even under the circumstances, its forecasts were good in the early years. Over the past four years, its forecasting has improved further. It's likely that this comes from learning from its past loans, and from gradually hiring more and better trained people in key positions.

RateSetter forecasts around 1.8% of the loans it has approved in 2019 will at some point be written off.

That is not an annual figure, but the total amount over several years. This means the 1.8% losses are one-off. Whereas lending rates of up to 2.0% are earned until loans issued in 2019 have eventually been repaid.

Provision Fund cover

Expected losses are more than covered by the RateSetter Provision Fund.

RateSetter expects to cover all bad debts plus having an extra 15% to 20% cover on top. Analysis of the data shows that RateSetter's expectations seem reasonable.

How the RateSetter Provision Fund works

The RateSetter Provision Fund is funded by payments from borrowers. About one-third of this is pre-funded. The rest is paid in each month, as part of the borrowers' repayments are diverted into it. The size of the payment for each loan depends on how risky it is.

When a loan falls late, the Provision Fund ensures that all lenders in the loan continue to receive the full amount they expect. If a loan falls beyond late and becomes a bad debt, the Provision Fund takes on the full bad debt. It then pays off the lenders who had the bad debt, including interest.

If RateSetter later recovers any of the bad debt, those recoveries could sometimes be added to the Provision Fund to protect lenders in future.

What happens if bad debts become larger than the Provision Fund?

Lender interest, combined with the existing Provision Fund, is currently a very strong barrier against lenders actually losing money.

If bad debts become much worse than expected, RateSetter will need to top up the Provision Fund. It first does this by reducing the interest rates that lenders have been earning.

It does this proportionally. For example, if RateSetter needs to take a fifth of your interest to top up the Provision Fund, those earning 4% would earn 3.2%. And those earning 3% would earn 2.4%. Lenders in the higher-earning accounts will therefore continue to earn more interest.

However, if the situation deteriorates too far, there wouldn't be enough interest to cover bad debts. Lenders would then all lose some money, as RateSetter will need to take a portion of the lent money to prop up the Provision Fund.

If that happens, all lenders will lose the same amount. So, for example, lenders might all lose 1% of the money they have on loan.

In the unlikely event you do lose a small proportion of your money, you can expect to recover quickly in the following months as the bad-debt situation improves.

How easy is it to lend?

Under the bonnet, RateSetter is complex. But for lenders it's made very simple.

You either upload money or set up a regular payment, or both.

You select whether to invest in the Access, Plus or Max account. You can lend through those accounts as IFISAs instead – or as well. It will take you a few extra minutes of form-filling.

RateSetter will then lend your money. And it will re-lend it as you receive your money back and interest from borrowers.

Unusually, re-lending your money is not optional, but mandatory. This is new since the last RateSetter review. While the lack of choice grates, I think this is probably a positive thing, on balance.

It enforces better investing discipline on lenders, because it reduces the risks even further if you re-lend money regularly. This is especially the case if you lend before, through and after a recession. You'll earn more interest to offset bad debts.

Is RateSetter good compared to savings accounts and cash ISAs?

| Comparison | Top account | Top “big-brand” account | Access | Plus | Max |

| Savings | 5.00%

(Post Office) |

[MoneySavingExpert3YrSavingsBrandRate]

([MoneySavingExpert3YrSavingsBrand]) |

1.5%

(+0.10%) |

1.75%

(+0.35%) |

2.0%

(+0.60%) |

| Cash ISAs | 4.60%

(Castle Trust Bank) |

[MoneySavingExpert3YrISABrandRate]

([MoneySavingExpert3YrISABrand]) |

1.5%

(+0.40%) |

1.75%

(+0.65%) |

2.0%

(+0.90%) |

The table above shows that RateSetter's interest rates currently beat the best savings accounts by +0.10% to +0.60%, depending on which lending account you choose. The difference is greater if you prefer savings accounts with a known brand name.

RateSetter's IFISAs beat cash ISAs by a greater margin, as shown in the table. The difference is +0.40% to +0.90%.

You may not know this, but interest is tax free for most people using savings accounts or peer-to-peer lending accounts. Unless you have a very high income or a large pot of money in savings and/or P2P investments. This is all down to the Personal Savings Allowance. You can read more in How Is Peer-To-Peer lending Taxed?

Based on these comparisons, I find the Max account attractive. The Access account doesn't add a great deal over the safer savings options. I barely see the point of Plus, since it fits in such a small space between Access and Max.

Savings and ISA rates in the table above come from MoneySavingExpert.1

How does RateSetter compare to the stock market?

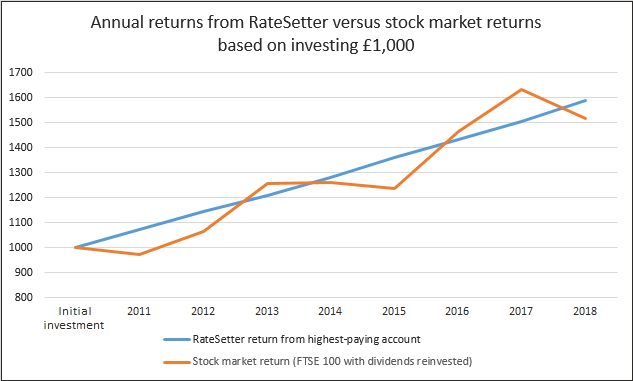

RateSetter has soundly beaten the stock market in both key ways:

- Lenders choosing its highest-paying accounts have earned more than the average investor in shares. They have outperformed the stock market.

- Lenders have earned a better risk-adjusted return – and can expect this to continue in future. That means RateSetter wins based on the reward you earn versus the risks taken.

1. Outperforming the stock market

Looking at all RateSetter's complete years of operating, investors in its highest-paying account have made 61.2% total returns. Over the same period of 2011-2018, the stock market's total returns were 51.5%, according to Schroders Data.2

It remains to be seen whether RateSetter will continue to outperform the stock market in terms of making more money. But, over the very long run, this isn't likely. Over time, investors tend to learn better what reward is fair for the risks. The reward shrinks – or rises – to meet expectations. With rates having come down recently, we are now within a range of fair value.

2. Better risk-reward balance than the stock market

On the other hand, RateSetter is almost certain to continue to outperform the stock market on risk-adjusted return. And that's over the short-, medium- and long-term.

Such is the nature of money lending that it provides a stable income, as the banks have learned over many decades – even centuries.

RateSetter's performance in this space has indeed been higher and more stable than the high-street banks, based on the most recent data we have (which is from when RateSetter began up to 2015).

And during RateSetter's eight full calendar years of constant profits, the stock market flatlined for two years and ended up lower three times.2

The graph above shows the bumpy results of the stock market. RateSetter returns look like a straight line upwards to the naked eye.

I don't know how often RateSetter will beat the stock market in pure rewards. But I am sure that it will continue to provide much more stable returns and better risk-adjusted returns.

Which RateSetter lending account is best?

I see almost no reason why anyone would choose to use Access or Plus, when you can earn more interest at the same risk through Max, with just a slightly higher exit cost. The Max account and Max IFISA are the best accounts RateSetter has to offer.

RateSetter lending review: lending tactics

Tactics when rates are falling

If lending rates are falling, my first tip is to keep checking how they compare to savings rates. Even with RateSetter's substantial defences, it could reach the point where there seems to be little reason for taking any risk. We're already in that ballpark for the Access account.

4thWay will help you keep on top of this. We send you email alerts, if you subscribe, when there are changes that we think should influence lenders' decisions.

Tactics to earn more money when rates are stable or rising

It's not easy to earn more than your peers. RateSetter has steadily weeded out opportunities to “beat” other RateSetter lenders.

Nevertheless, I have three suggestions if you want to offer higher than the going rate in an attempt to make small improvements to it:

1. Wait till your money has been lent once already

When RateSetter queues lenders' money, it prioritises money that's waiting to be re-invested (re-lent).

This suggests a strategy for those of you who want to attempt to earn higher rates. Lend at RateSetter's going rate (advertised rate) initially. Then switch to your own, chosen higher rate after your money has been lent out for the first time.

2. Aim to lend around the 21st of the month

Some old RateSetter data suggests that lenders might be able to lend at slightly higher rates around this date more easily. Look to lend around the 21st of each month to hit the spike.

The small spike might be caused by borrower demand being roughly even throughout the month, but lender contributions clustered more around paydays at the start and end of the month.

Even if you're using the going rate, by timing your payments here you might lend your money a little more quickly.

3. Count the days

See how long it takes you to lend at higher rates. For every +0.1% that you earn, it should take you no more than five working days to get your money lent. If it takes longer, you might end up worse off.

How can I use the RateSetter website?

RateSetter no longer publicly shows the characteristics and results of every loan it's ever approved, although 4thWay receives this for its detailed analysis and bank-type stress tests.

However, it does provide a huge amount of clear information and statistics for lenders through its website.

RateSetter's main statistics page

The top section of RateSetter's main statistics page* gives you some key figures. This includes the total amount ever lent, the total on loan now (total “under management”) and even the amount that lenders have successfully sold to other lenders (“sell outs”) when they needed their money back.

The investor returns section gives you figures on how much money RateSetter lenders have made over the years. This section is based on average returns across all its lending accounts. The figures might nicely add to your understanding, because in my RateSetter review, most of my own statistics are around the highest-paying account.

The lending volume graph might help you to better visualise how loans are gradually paid off over the years. So much so, in fact, that I shall pinch it, here:

Image correct as of December 2019.

The remaining sections on the page give you a lot of facts and figures about the RateSetter Provision Fund. You can get additional information about it on this page.

Lending returns and what you're investing in

If you'd like to see RateSetter's own calculations comparing it to the stock market, you can get it on this page.

You can also see the mix of loans currently on offer. On this page, RateSetter calls its small business loans “asset” loans.

RateSetter pages about their people

RateSetter's main page about its key people contains sparse information, but even that gives you a good flavour. In my experience and that of my colleagues, a good number of peer-to-peer lending platforms greatly – or gravely – exaggerate the skills and experience of their people in their online profiles. 4thWay can confirm that this is not the case at RateSetter.

You might also read this article from the person who has the most responsibility for ensuring your money goes into good loans and that enough money goes into the Provision Fund.

RateSetter's lending standards

I recommend you read about lending standards from RateSetter. It might be useful to compare them against other peer-to-peer lending or IFISA platforms that you're considering lending in. The key page is here.

How much are RateSetter lending fees?

In peer-to-peer lending, the total cost to lenders is the difference between what borrowers pay and what lenders get. This is called the “spread” or “margin”.

In the case of RateSetter, the picture is a little more nuanced. A good portion of what the borrower pays goes into the Provision Fund to protect lenders.

RateSetter is leading the way on transparency. It's one of very few P2P lending companies that now provides enough information for us to tell you how much they cost you.

Unfortunately, almost all other peer-to-peer lending and IFISA providers don't reveal the size of their fees. The most common reason for this secrecy is that peer-to-peer lending platforms don't want competitors to find out what their margins are. They are concerned that doing so will start a price war.

How much RateSetter costs

RateSetter publishes total borrowing costs over the past 12 months. The average cost to borrowers has been 11.3% and lenders have received an average 4.3%, although that excludes the temporary halving of lending rates during COVID-19 time.

A substantial 4.0% of the lent amount went to the reserve fund. Again, COVID-19 has seen a temporary boost to that figure which is not taken into account here.

Therefore, RateSetter's fees including the reserve fund were 7% and, excluding that, they were more like 3%. This is at the lower end of what I had expected before RateSetter started to publish its lender costs. So it's a fair price for the kind of lending RateSetter offers.

Don't underestimate the value of this information. Normally we have to estimate it from scraps of information. I think it could say a lot about RateSetter's faith in its business and loan modelling that it's prepared to reveal this.

Is RateSetter regulated by the FCA?

RateSetter is regulated by the UK's financial regulator, the Financial Conduct Authority.

As with all FCA-regulated businesses, you may submit complaints to the Financial Ombudsman Service – a powerful consumer body – if you feel that RateSetter has treated you badly.

Is RateSetter covered by the FSCS?

If you lose money on any kind of investment, the government doesn't compensate you through its Financial Services Compensation Scheme. Peer-to-peer and IFISA lending is a form of investment, so the same applies here. Lending through RateSetter is not covered by the FSCS.

However, RateSetter has a segregated account for lenders' unlent money at Barclays Bank. When any of your money is held in that account, it's covered under the bank's FSCS. That's in the event Barclays goes out of business.

Any money you have in other Barclays Bank accounts, including in cash at RateSetter, is covered under the same limit. Barclays Bank shares its banking licence with Barclays Wealth Management, so savings in that business count towards your FSCS limit as well.3

Read Which P2P Lending Sites Offer FSCS Protection? to find out where your unlent cash receives protection.

What if RateSetter goes bust?

If RateSetter goes bust, it has a fully-funded plan in place to ensure that loans wind down smoothly. Lenders will continue to receive repayments and interest. And the Provision Fund will continue to pay out and to chase bad debts.

Most importantly, if RateSetter were to shut down, your borrowers still owe you. Their repayments can't be diverted to pay off RateSetter's debts.

I consider it unlikely that lenders will lose money as a direct result of RateSetter's closure. Any losses are likely to be very small; I expect the annual cost of administering run-off loans to be about 0.5%-2.5% of the outstanding loan book. All offset by interest earned.

Investing in RateSetter

You might wonder about investing in RateSetter itself by buying shares in its business. That's in contrast to lending through its online platform.

Unfortunately, just like most peer-to-peer lending websites, RateSetter is not yet public – i.e. not listed on the stock market. Buying shares is not yet an option.

If it ever becomes possible, 4thWay will cover that in a separate RateSetter review on buying its shares.

Summary of the investing tips in this RateSetter review

- Use the Max account and/or Max IFISA to get the best risk-reward balance.

- Lend more money regularly to reduce risks.

- Use RateSetter as one of at least six peer-to-peer lending websites in a portfolio.

- Put no more than 30% of your total investing pot into RateSetter.

- Subscribe to 4thWay to keep track of RateSetter.

RateSetter review: my conclusion

If I had to choose one peer-to-peer lending platform that everyone with savings must put money into, I think it would be RateSetter.

It's well established, has an excellent record and great people, a large reserve fund, incredible diversification, and bad luck from bad debts is eliminated because all lenders get the same return.

Lenders like RateSetter

RateSetter has no obvious direct competitor. No other peer-to-peer lending site offers a similar blend of loans, the same flavour of risk and reward.

I would say that because of its personal loans, it's most like Zopa. They also share the fact they are giants compared to most platforms. Read the 4thWay Zopa Review.

On the property development lending side, there are no peer-to-peer lending websites or IFISA providers that have both RateSetter's scale and record. I would suggest this side is most similar to Octopus Choice. Octopus's property loans are different to RateSetter's, mostly being rental properties and short-term (bridging) loans.

However, here are the similarities:

- Octopus is also here to stay, as it's backed by the huge Octopus Group.

- It makes it easy to invest, as the minimum lending amount is £10.

- It completes a lot of loans.

- Your money is spread out across a basket of them.

- Its record on bad debts is also good, although it's not as transparent with us as RateSetter.

Thank you!

Thank you for reading the RateSetter review, and well done for making it to the end!

Visit RateSetter.

Articles, guides and reviews that were mentioned in this review

About the 4thWay PLUS Ratings and 4thWay Risk Scores.

How Is Peer-To-Peer lending Taxed?

Which P2P Lending Sites Offer FSCS Protection?

Why Do Peer-To-Peer Lending Rates Fall? 5 Reasons.

P2P Lending And IFISA Cashback Deals Available Now.

For your education

Personal Peer-To-Peer Lending: It's Underrated!

Independent opinion: 4thWay will help you to identify your options and narrow down your choices. We suggest what you could do, but we won't tell you what to do or where to lend; the decision is yours. We are responsible for the accuracy and quality of the information we provide, but not for any decision you make based on it. The material is for general information and education purposes only.

We are not financial, legal or tax advisors, which means that we don't offer advice or recommendations based on your circumstances and goals.

The opinions expressed are those of the author(s) and not held by 4thWay. 4thWay is not regulated by ESMA or the FCA. All the specialists and researchers who conduct research and write articles for 4thWay are subject to 4thWay's Editorial Code of Practice. For more, please see 4thWay's terms and conditions.

The 4thWay® PLUS Ratings are calculations developed by professional risk modellers (someone who models risks for the banks), experienced investors and a debt specialist from one of the major consultancy firms. They measure the interest you earn against the risk of suffering losses from borrowers being unable to repay their loans in scenarios up to a serious recession and a major property crash. The ratings assume you spread your money across hundreds or thousands of loans, and continue lending until all your loans are repaid. They assume you lend across 6-12 rated P2P lending accounts or IFISAs, and measure your overall performance across all of them, not against individual performances.

The 4thWay PLUS Ratings are calculated using objective criteria that can be measured and improved on over time, although no rating system is perfect. Read more about the 4thWay® PLUS Ratings.

Our service is free to you. We don't receive commission from the above-mentioned companies. We receive compensation from some other P2P lending companies when you click through from our website and open accounts with them. This doesn't affect our editorial independence. Read How we earn money fairly with your help.

1To get savings account rates for the RateSetter Review, I used this page of MoneySavingExpert. To get cash ISA rates, I used this page. I chose accounts paying fixed rates for three years, because it compares well to a typical, sensible lending period.

2You can see the data from Schroders publicly in this Cazenove article. In the RateSetter Review, I have assumed that the total costs of investing in the stock market have been 0.5% per year, which is very low. For those of you who know about investing in shares, I assumed investors re-invested dividends, which increases investors' profits.

3Banking licence information taken from here.