CapitalStackers Review

Attractive opportunities for active lenders to pick high-quality loans with very large profit potential

CapitalStackers’ Property Lending Account/IFISA has earned an “Exceptional” 3/3 4thWay PLUS Rating.

We forecast that lenders who start lending today will earn an average 13.49% interest after bad debts, most of the time, although this will vary depending on your specific loans.

Visit CapitalStackers* or keep reading the CapitalStackers Review.

What does CapitalStackers do?

CapitalStackers* mostly does development loans with its lenders normally taking the junior position. This means that other lenders will get their money back first if the borrower struggles with the development and with loan repayment.

The loans at CapitalStackers are often very junior, which is called mezzanine finance, and even sometimes the rarer, most-junior kind of development lending possible, which is called stretch finance.

CapitalStackers also does some bridging loans to support developers.

When did CapitalStackers start?

CapitalStackers matched its first P2P loan in March 2014. Lenders have now lent £47 million.

What interesting or unique points does it have?

CapitalStackers’ offers some of the highest interest rates available, averaging 13.49%.

It puts it fees on the line first, losing them if a loan is not to be repaid in full.

The directors and close family have always lent a large amount of money in the same loans through its online lending platform. Still today, they do 20% of the lending, firmly putting their wealth on the line: £4 million.

While they lend in all loans, their own weighting is slightly towards the riskier side – including on the loans that have recently been suffering the most issues or even had write-offs.

In some cases, the directors put in extra cash by themselves to get a troublesome development over the line.

Some wealthy or sophisticated lenders are invited to join its “underwriting club”. Those in the underwriting club are allowed, if they wish, to take part in the riskiest “stretch finance” part of any loans that need it. CapitalStackers directors and families also take part in the stretch finance.

When you buy or sell existing loan parts, you’re allowed to do a deal with other lenders to conduct the trade at a massive mark-up or discount, depending on how urgently you want to get the deal done and the condition of the loan or development project. That is most unusual in P2P lending.

Instead, normally, you sell the loan at its original value and you’re not allowed to sell any loans suffering any kind of problems.

To me, it means that only people who take the time to understand what they’re doing and are able to keep cool heads should lend through CapitalStackers, because you’re otherwise liable to do the wrong things, such as panic-selling for a big loss.

How lending works at CapitalStackers

These loans take a little explaining.

CapitalStackers focuses on an interesting area that is still less common in P2P, and where other providers have had hit-and-miss results.

You mostly provide the additional cash over and above that provided by banks to complete developments.

The banks used to offer these loans too, but pulled back considerably since the Great Recession, leaving developers short of the funds they need to get developments completed. They now much prefer to focus on the safer, lower-rate “senior debt”.

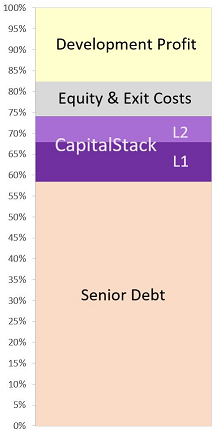

“CapStack” lenders might typically put their cash down first, e.g. to assist a property developer in buying the land. Yet you’ll normally not be first in line for being repaid in the event a loan goes bad. So you’re behind another lender – or other lenders.

CapitalStackers splits its loans into as many as five layers.

If you’re in layer one, you’ll be repaid second behind the senior lender (usually a bank) in the event that a borrower struggles to repay all its debts on the development project in full. If there’s no external lender, you’ll be repaid first.

If you lend in layer two as well (or instead), you’ll get higher rates for it but you are again in a worse position in terms of risk, getting back your money after the senior lender and layer one lenders are repaid in full. This pattern repeats all the way up to layer five, if you choose to take part.

As a result of all this, CapitalStackers* agrees to pay out considerably more interest in all layers than you normally get in P2P development lending.

CapitalStackers review: how good are its loans?

Loans typically hit 70% to even 80% of the hoped-for sale price of the completed development. That is, with all layers of a loan combined, including any senior debt held by a bank.

That said, there are a lot of ways to slice up loans to measure risk – especially when loans are stacked and layered the way they are at CapitalStackers.

The primary way (although not the only way) to slice up risk in this case is to consider each layer of each loan as a separate loan by itself. Which means for core modelling we can reduce the five layers into two categories of loan at CapitalStackers:

Category 1 loans) This is layer one of any CapitalStackers loan when it is the senior loan, i.e. there is no external funder taking the senior part of the loan. In this event, you’ll get your money back first if the loan turns bad and the bad debt needs to be recovered through whatever possible means.

The average interest rate on category 1 loans has been 8.80%. The amount lent here compared to the hoped-for sale price is just 38.48%. That’s very attractive compared to senior development lending elsewhere.

Category 2 loans) Everything else is in this category – and that is about 80% of all the lending done on CapitalStackers.

Each layer of every loan from layers two to five should be considered a distinct category two loan for core risk assessment. In addition, category two includes layer one loans that are not the senior debt, because a bank is funding the senior part.

Again, taking each of those layers in each loan as a unique, individual loan itself, we find that the average interest rate is 14.33%.

We also find that the risk to you, on average, kicks in at 66.76% of the hoped-for sale price. Plus, the average amount lent on all lending that is senior to it is 60.26%. It’s this narrow window between the two that is a hidden reason why layered mezzanine and stretch development lending is intrinsically riskier.

And that’s why rates are so much higher: sometimes 20% or even more in the higher layers.

To demonstrate the point on risk, consider two hypothetical property loans. The first is a loan to the property owner for the full amount needed, at 75% of the expected sale price.

The second loan you make is mezzanine, whereby an external, senior lender is lending 65% and you’re topping that up to 70%. Note that what the borrower received is less in this second loan when compared to the property valuations.

Now let’s say there’s a severe downturn and through some rough bad luck both properties are sold for a return of just 66% of the properties’ expected sale prices.

In the first loan, the lender got back 66/75 = 88 pence in the pound.

In the second loan, you as the junior lender got back just 1/5th – or 20 pence in the pound – even though you were not pushing the total lent to the borrower as much as in the first loan.

Bear in mind that the upper-most layer in loans with three to five layers can include a proportion of lending that only CapitalStackers directors, their families, and members of its underwriting club are allowed to choose to take part in.

They typically do the lending at or above 75% of the properties’ valuation, according to CapitalStackers’ data.

However, CapitalStackers, in its usual cautious way, uses a unique measure that overstates that amount. I estimate that most lenders really are being capped at a maximum of about 72% of the hoped-for sale price.

Current events: the conclusion of a major property development downturn

On CapitalStackers loans that you start lending in from today – taking each layer as a separate loan – I estimate your returns are likely to be closer to the long-term average of 13.49%.

That is distinct from the return that is expected on historical loans outstanding. CapitalStackers does the intrinsically riskiest kind of lending to property developers, more so than any other P2P development lending provider.

And those developers – who sort of started their projects from 2021 to 2023 in particular – have just been going through some of the worst possible conditions for housebuilding imaginable.

Property developers – and by extension their lenders, like you – faced a remarkable wave of setbacks, the effects of which are now coming to a peak.

The departure of skilled construction workers as Brexit took hold was sharply worsened by the pandemic. Supply chains broke down, inflation drove up material costs, and in autumn 2022 interest rates spiked, crushing buyer demand and leaving developers struggling to sell properties quickly.

This is unquestionably the equivalent of our worst-case modelling we at 4thWay do, when we use a stricter version of the stress tests that global banks are required to do on their loanbooks.

CapitalStackers is unusually cautious in terms of reporting potential losses (as in everything else it does), so it’s still too early to say how the dust will completely settle. However, the picture is solidifying, as most of the loan amounts that were considered in danger were written off by the last day of 2025.

A weighty 8% of all amounts ever lent have become confirmed losses or have been provisioned for probable loss. That nearly matches the mighty average lending rate paid to lenders, which has been just above 13% per year, which is usually earned for close to two years.

To put it mildly, it was a very rough patch. For lenders who put a lot more money into loans three to five years ago than at any other time, their losses might be even higher.

The directors and other connected parties have taken the brunt of those losses. They have probably lost around 50% more than the average lender. The underwriting club members will also have taken more of the brunt.

Nevertheless, based on 4thWay models, I still expect that most lenders who took on a decent spread of loans and layers during the worst possible two-year period of this developer downturn will still ultimately earn a positive return. Many of those loans have already repaid in full with interest.

CapitalStackers’ own figures show interest earned or paid out after bad debts and allowing for strict provisions for potential bad debt on all its live loans is still substantially higher than its write-offs. In other words, the live loans pay for themselves and the average lender is not reliant on their huge past earnings through CapitalStackers to stay in the black.

One more point to add is that CapitalStackers calls loans write-offs earlier than most other property lending platforms. Between 10% and 70% of the amounts it has written off or provided for as future write-offs could still, even at this late stage, be clawed back.

How much experience do CapitalStackers’ key people have?

CapitalStackers’ team is right up there as one of the most competent we have seen. It has many decades of relevant banking experience, it has high standards, including ethical standards, and it does appropriate risk modelling using professional firms. It covers all the bases.

When borrowers have suffered any issues, CapitalStackers has proven themselves to be talented at finding ways to help developers get their projects completed and the properties sold.

I’m very happy to have these people providing high-interest investments.

CapitalStackers review: lending processes

CapitalStackers works closely with high-street and specialist banks to arrange the deal, where the bank is the senior lender and CapitalStackers’ lenders are the junior ones. It appears to have built some good working relationships, which can be very useful in getting agreement on how to deal with development projects that are struggling to ensure that all lenders get the most out of it in the end.

Funding for developers is fully arranged in advance and disbursed in phases. At some P2P lending companies, there’s the risk that a developer completes part of a project, but then the money dries up for the remainder of the development work, because it’s not been fully agreed or raised in advance. So I like seeing that it’s all settled up front.

All the development loans have planning permission. As well as using its own considerable experience, CapitalStackers gets independent valuations on all properties and developments.

CapitalStackers* takes diligence in assessing loan applications, and monitoring loans and developments, to a whole new level – beyond the comprehensive assessments we would usually expect for these kind of complex, high-interest loans.

They understand what makes a good borrower – a good property developer – and have a far better understanding of the numbers than we usually expect – or even require – to see for these sorts of loans.

Their expertise has enabled them to help developers to complete projects and sales when unexpected issues have arisen. CapitalStackers has shown the skill and ingenuity that we would hope for in responding quickly and helping the developers get their projects back on track.

Plus, CapitalStackers builds in an enormous runway in case of development or property sale delays, or higher costs.

How good are CapitalStackers’ interest rates, bad debts and margin of safety?

The mine of data that CapitalStackers provides us with is the most varied and detailed that we receive by a long margin. Boy, do they take data seriously. Now that it has enough history for much more analysis to be meaningful, it will take some time before we can work out how to use a lot of it.

But, with the help of our in-house software, I have distilled the most important information. To that end, we have been able to conduct our core stress tests to assess CapitalStackers for a 4thWay PLUS Rating, as its history has now become sufficient for us to do so. It has earned the top rating of 3/3, since we strongly expect that in major downturns, like the one its developers have just been going through, lenders overall will still make money, due to sufficient interest covering any losses.

Our modelling also finds a 7/10 4thWay Risk Score. This means that, before any interest you earn, losses can potentially exceed 15% on loans issued in a downturn period. That’s not 15% per year but 15% as a one-off, over all years the loans are being chased. Therefore annual interest in the good loans helps to offset that.)

So, the 4thWay PLUS Rating out of three incorporates interest earned to offset losses, while the 4thWay Risk Score only looks at the losses, with no offset.

This 4thWay Risk Score result is hardly surprising for mezzanine development lending. Indeed, for lenders in the underwriting club and for the directors of CapitalStackers itself, the 4thWay Risk Score would likely be bumped up to at least 8/10.

For all the above analysis to make sense to you as an individual lender, you need to take responsibility for having a sensible strategy, which means spreading your money fairly evenly across lots of loans or layers, although weighting lower layers somewhat more than higher ones.

You also must bear in mind that the 4thWay PLUS Ratings assume that you lend across 6-12 rated accounts, since any one basket of loans for any one lending account can potentially shock more than any of us expected. In other words, it’s the basket of rated accounts that count!

All loans issued in CapitalStackers’ first nine-and-a-half years, from 2014 onwards, were fully repaid with full interest. Some of those loans went very late, but those delays are normal and expected in most development lending even in good times. And the proportion of loans going very late was well within sensible bounds.

Interest earned by lenders so far already amounts to four times the lent amounts that have been written off.

Has CapitalStackers provided enough information to assess the risks?

CapitalStackers is exceptionally transparent with 4thWay. It provides a huge amount of access to its people and supporting information. It goes so far as to give us the information it submits to the financial regulator and a whole lot more, giving me a lot of confidence.

With lenders, too, CapitalStackers now provides pretty clear and comprehensive statistics, and it does its best to explain how these complex loans work.

I would encourage you to give the decision makers a call to discuss their statistics and individual loans; it’s an opportunity you can’t get with all P2P lending providers.

Is CapitalStackers profitable?

CapitalStackers* is already profitable and indeed it has been for closing on a full decade now. It’s a small business but with very low costs, making it seemingly easy to sustain.

It has backing from an accountancy firm. It has a network of connections that we believe will enable it to expand and grow further, offering more loans as more lenders are attracted to it.

What can you tell me about CapitalStackers’ cybersecurity?

A soft security probe of CapitalStackers’ lending portal finds it to be in good health with no apparent malware. It is marked clean by Sucuri, Google Sage Browsing, McAfee and other internet and security technology providers.

CapitalStackers’ website is secure and it automatically directs you to a secure version of its site.

Its website technology is up-to-date and it runs a firewall to monitor and if necessary block information going into and out of the website.

Is CapitalStackers safe and a good investment?

If you want to choose just one potentially very high-return investment for your lending and investing portfolio, CapitalStackers* could be the one.

An extremely professional business and with heart to go with it – you’ll find few borrowers or lenders who feel let down by CapitalStackers.

What is CapitalStackers’ minimum lending amount and how many loans can I lend in?

The minimum lending amount at CapitalStackers is £2,500 in each loan, which is high compared to most P2P lending companies. When you’re buying second-hand loans from other lenders, the minimum drops to £500.

CapitalStackers currently approves relatively few loans, but you don’t have to transfer money until the loan is fully sold. You’ll need to take a lot of months to spread your money across more loans.

Does CapitalStackers have an IFISA?

Yes, CapitalStackers has an IFISA.

Can I sell CapitalStackers loans to exit early?

Yes, you can sell your loans to other lenders, if they want to buy. CapitalStackers doesn’t charge for this, although it reserves the right to do so in future.

As the development progresses, the certainty of successfully completing the project increases. Therefore, with CapitalStackers’ loans, the risk of losses falls considerably as the months go by.

As a result – at least in normal times – you can often sell your loans for more than you paid. The lender who buys your share effectively gets a lower interest rate that better fits the lower risks, and you increase your total profits.

What else do you need to know?

Starting from summer last year, in 2025, CapitalStackers has changed the order of payments from loans with the most severe issues.

Interest payments are now frozen for all lenders in all layers of a loan, as soon as CapitalStackers has established that some level of write-offs of the amount lent are likely to occur in any of the layers. It freezes the interest in this way before establishing what actual amount will finally be written off, when all efforts to recover the debt are over.

It’s unusual in property lending for lenders in safer, lower layers to share the risk in this way, regarding losses of interest with those higher up the stack (Normally, payments from the borrower would first pay the interest to the safest layer, then any additional payments would go towards the actual debt in the safest layer. Then it would progress to the next layer, interest first then the actual debt. And so on.)

However, the lowest layers still do continue to receive all the payments made by the borrower first, until the actual lent amount is repaid, before anyone higher in the stack will receive a penny. It’s just that no-one will benefit from earning any further interest until the entire loan amount of all layers has been repaid.

Independent opinion: 4thWay will help you to identify your options and narrow down your choices. We suggest what you could do, but we won't tell you what to do or where to lend; the decision is yours. We are responsible for the accuracy and quality of the information we provide, but not for any decision you make based on it. The material is for general information and education purposes only.

We are not financial, legal or tax advisors, which means that we don't offer advice or recommendations based on your circumstances and goals.

The opinions expressed are those of the author(s) and not held by 4thWay. 4thWay is not regulated by ESMA or the FCA. All the specialists and researchers who conduct research and write articles for 4thWay are subject to 4thWay's Editorial Code of Practice. For more, please see 4thWay's terms and conditions.

The 4thWay® PLUS Ratings are calculations developed by professional risk modellers (someone who models risks for the banks), experienced investors and a debt specialist from one of the major consultancy firms. They measure the interest you earn against the risk of suffering losses from borrowers being unable to repay their loans in scenarios up to a serious recession and a major property crash. The ratings assume you spread your money across hundreds or thousands of loans, and continue lending until all your loans are repaid. They assume you lend across 6-12 rated P2P lending accounts or IFISAs, and measure your overall performance across all of them, not against individual performances.

The 4thWay PLUS Ratings are calculated using objective criteria that can be measured and improved on over time, although no rating system is perfect. Read more about the 4thWay® PLUS Ratings.

*Commission, fees and impartial research: our service is free to you. 4thWay shows dozens of P2P lending accounts in our accurate comparison tables and we add new ones as they make it through our listing process. We receive compensation from CapitalStackers and other P2P lending companies not mentioned above either when you click through from our website and open accounts with them, or when you make an investment, or to cover the costs of conducting our calculated stress tests and ratings assessments. We vigorously ensure that this doesn't affect our editorial independence. Read How we earn money fairly with your help.