See why 4thWay now accepts ethical ads.

See why 4thWay now accepts ethical ads.

Funding Circle’s Christmas Cashback Loans

Funding Circle is currently returning cashback to lenders, taken out of the borrowers’ fees, in a few select loan auctions.

The loans are listed as A+, which is Funding Circle’s highest borrower grade. Although Funding Circle conservatively estimates that 0.6% of these loans will go unpaid each year, barely a dozen A+ loans out of more than 1,000 have gone bad since Funding Circle started in 2010.

Average annual interest for lending to A+ loans without cashback is currently around 7.9% after fees. All the following cashback loans pay 6% or 7%, plus 1% cashback, so they're in the same ball park.

You get paid cashback straight away, untaxed, and so you can lend the whole lot immediately to earn even more interest. You also can't lose it due to a loan going bad.

A+, Residential property mortgage for 16 months in Hammersmith, London

- 7% fixed interest, which is an estimated 6% after Funding Circle fees.

- Cashback of 1% on top.

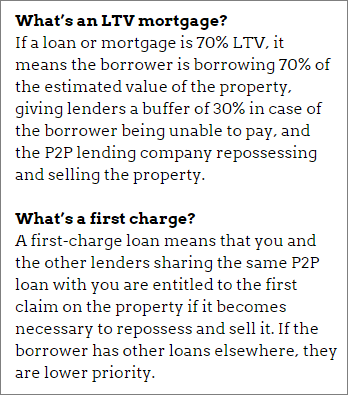

- 58% LTV mortgage with a first charge.

This loan, and all others in this article today, are fixed rate loans that you can lend to on a first-come, first-served basis. That means that once the loans are fully funded, you can't bid lower interest rates to steal loan parts from other lenders before the auction closes.

The auction finishes at 4.34pm on Tuesday 23 December at the latest.

£102,000 of this £110,000 loan has already been funded.

This is an interest-only loan, which means you’ll receive monthly interest payments and your actual loan will be repaid at the end, so you will get interest on the full amount of the loan without having to re-lend the loan itself – just the interest.

A+, Residential property mortgage for 13 months in Cornwall

- 8% fixed interest, which is an estimated 7% after lending fees.

- Cashback of 1% on top.

- 63% LTV mortgage with a first charge.

The auction finishes at 6.32pm on Friday 26 December at the latest.

£70,000 of this £200,000 loan has already been funded.

This is an interest-only loan.

A+, Residential property mortgage for 16 months in Newquay

- 8% fixed interest, which is an estimated 6.4% after fees.

- Cashback of 1% on top.

- 72% LTV mortgage with a first charge.

The auction finishes at 2.51pm on Monday 29 December at the latest.

£285,000 of this £400,000 loan has already been funded.

This is another interest-only loan.

*Commission, fees and impartial research: our service is free to you. 4thWay shows dozens of P2P lending accounts in our accurate comparison tables and we add new ones as they make it through our listing process. We receive compensation from Funding Circle, and other P2P lending companies not mentioned above either when you click through from our website and open accounts with them, or when you make an investment, or to cover the costs of conducting our calculated stress tests and ratings assessments. We vigorously ensure that this doesn't affect our editorial independence. Read How we earn money fairly with your help.