Tesla Bonds Prove P2P Lending Is Safer Investment

Many Tesla bond investors are complete lunatics.

Many Tesla bond investors are complete lunatics.

Today, I read on CNN that Tesla bonds have fallen in price so much that anyone buying its bonds due for repayment in 2025 will now effectively earn 8.6% annual interest.

(A falling price for selling your bonds leads to a higher effective interest rate for the buyer.)

I can’t tell you how crazy it is that investors are still happy to earn a mere 8.6% on these bonds.

No, wait. I can tell you. And it is a great example of why people interested in lending should consider swapping out of bonds and into peer-to-peer lending.

A startup funded with lots of debt

To start with, in Tesla you’ve got a business that is mostly focused on manufacturing cars. The automobile industry has produced amazing innovations for transport and humanity, but notoriously dreadful long-term results for investors. Proving that great products and making money do not go hand in hand.

Although Tesla was founded in 2003, it is still in startup mode, having made consistent losses in its attempt to build itself into a profitable car manufacturer.

Figures from Macrotrends back to 2008 show a loss every single year, with the smallest loss being $74 million in 2013 and the largest was $2 billion in 2017. This year, the losses will probably be even bigger.

Yet, before it has got anywhere near producing positive rewards for its share investors, you have already got people lending billions of pounds to it.

8.6% – for this? Really?

Prior to the recent fall in the bond’s sale price, investors were earning around 5% interest. Some investors must have now sold their bonds for a loss after the resale price fell, even after factoring in the interest earned.

Investors are only now demanding interest rates close to double digits. It has taken the following to occur before this stage was reached:

- Losses every year.

- Forecasts regularly missed.

- A senior management exodus.

- CEO Elon Musk smoking pot live on air.

- CEO Elon Musk publicly calling financial analysts’ questions stupid and boring.

- CEO Elon Musk accusing a rescuer of being a paedophile on twitter.

- CEO Elon Musk admitting that he sometimes works as much as a psychotic 120 hours in a week, rather than choose people to delegate to. (That one’s my favourite; or it would be if it were not for the fact that his health and life are in serious danger.)

Those facts should send investors running even before looking at Tesla’s actual business model and $10 billion debt pile.

Investors initially bought these bonds before knowing all of that. Even so, they did know that it was a prospective business being built on debt in a highly competitive industry.

And I’m not even going to get into the fact that these are in the form of complex and obscure bonds called convertibles, which can take on a lot of the risks of share investing without necessarily offering the rewards.

You buy shares in startups – you don’t lend to them

With businesses like that, this is the time to be a share investor, not a bond investor.

As a general rule, businesses still trying to grow into a profit should not be lent to, even if it is 15 years old.

Investors, instead, should usually choose to buy shares in startups at attractive prices, so that they are able to align their potential rewards to the much greater risks involved. You’re not looking for 8.6% returns in investments like this, but for getting 10 or 20 times your initial investment.

Long-term investments with compressed interest rates

A defining characteristic of bonds is usually their long lives.

The specific Tesla bonds I’m writing about today are still not payable for another seven years. Investors are apparently either very comfortable that Tesla will be able to repay or renew the debt in seven years, or they see it as a Ponzi scheme where they can make a profit if they can just sell the bonds soon enough before the price collapses too far.

Another defining characteristic of many bonds is that money managers are practically forced to buy a lot of them, which puts downward pressure on interest rates.

Governments set the rules so that pension providers end up having no choice but to buy their government bonds, along with a load of company bonds. Plus, to counter the swings of the stock market, which perturbs many amateur investors, investment fund providers offer bonds to reduce any swings.

The money stuffed into bonds, in some cases rather like at gunpoint, pushes interest rates down.

As a result, history has repeatedly shown that bond investors can suffer very long periods of poor returns.*

What kind of long-term investment is designed where investors can often barely make a profit over the very long run, if they are lucky?

Why P2P lending beats bonds like Tesla’s

My title was a bit provocative. Tesla doesn’t completely “prove” that P2P lending is safer. But it is a very strong case in point that also helps me to highlight the weaknesses of the bond market in general.

Peer-to-peer lending does not have the same factors that ultimately force people to invest at marginal interest rates and therefore there will be less crazy acceptance of such poor interest rates.

With P2P loans usually having shorter horizons, there is no lazy assumption to fall back on that long-term loans must equal low interest rates.

You can earn around 8.6% with Tesla bonds if you want.

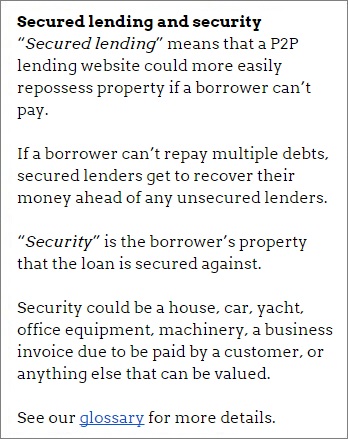

Or, instead, you can earn similar rates in P2P loans to very stable businesses that have been making profits for years and that often offer substantial security (see info box) valued at considerably more than the size of the loan.

A diversified portfolio of such loans offers an excellent risk-reward balance whether you want to lend for just a few years or for the long term.

Get started in P2P lending with 4thWay’s P2P Lending Guide.

Independent opinion: 4thWay will help you to identify your options and narrow down your choices. We suggest what you could do, but we won't tell you what to do or where to lend; the decision is yours. We are responsible for the accuracy and quality of the information we provide, but not for any decision you make based on it. The material is for general information and education purposes only.

We are not financial, legal or tax advisors, which means that we don't offer advice or recommendations based on your circumstances and goals.

The opinions expressed are those of the author(s) and not held by 4thWay. 4thWay is not regulated by ESMA or the FCA. All the specialists and researchers who conduct research and write articles for 4thWay are subject to 4thWay's Editorial Code of Practice. For more, please see 4thWay's terms and conditions.

*As usual for bond and equity research, 4thWay recommends the unparalleled Credit Suisse Global Investment Returns Yearbooks and Sourcebooks.

These show that, before costs, bond investors have frequently lost money after inflation over the long run, sometimes for as long as 30 years. Deduct costs and the time to recover inflationary losses will be considerably longer.