See why 4thWay now accepts ethical ads.

See why 4thWay now accepts ethical ads.

Future Reserve Fund Shock To Upset Many P2P Lenders

I’m going to explain some of the strengths and limitations of reserve funds.

Then I’m going to write about three simple steps you can take to give yourself the level of safety you probably want and have expected all along, to get yourself prepared for reserve fund failure.

Because on talking to several 4thWay users, it has become clear to me that there is a shock that they will receive, possibly in the not-all-too-distant future, due to a misconception they have about reserve funds.

It’s not their fault: the P2P lending sites need to do a lot better to explain it.

But these lenders are putting too much value on reserve funds and not enough on the other factors that the same P2P lending sites use to reduce risks.

Reserve funds are expendable – and sometimes will be fully spent! Other factors are much more important than reserve funds in protecting you from losses.

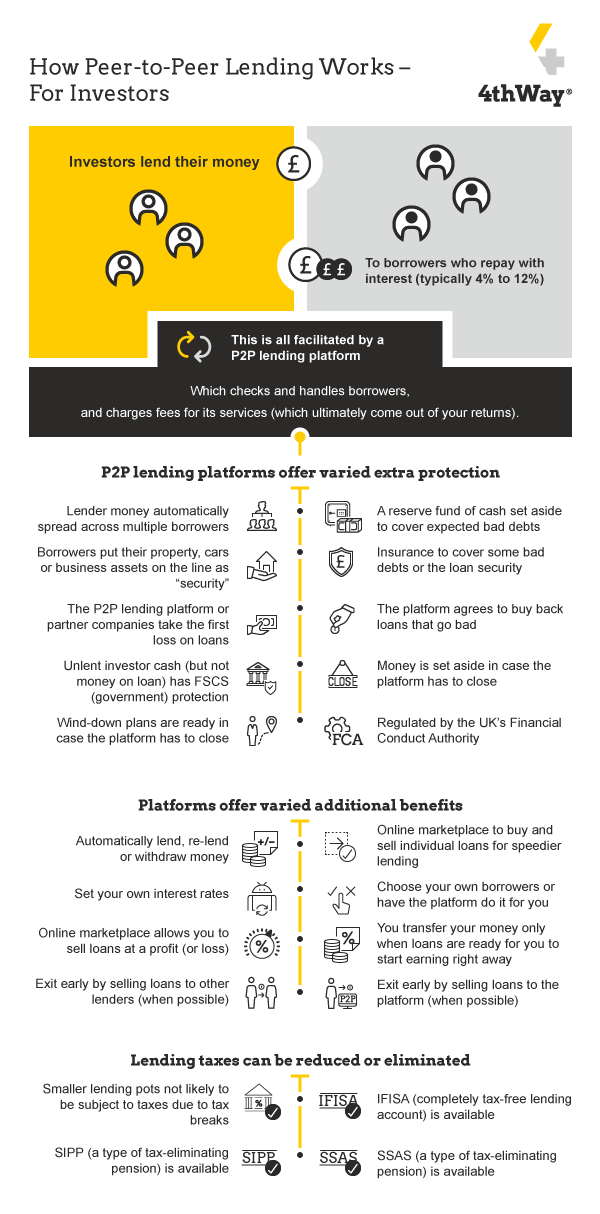

Reserve funds are not the main event

Lower-risk P2P lending has provided highly satisfactory returns to lenders.

Many of the P2P lending sites offering lower-risk options have reserve funds. Yet it is not due to the reserve funds that lenders have done so well. And it is not because of the reserve funds that lower-risk lending is safer.

The risk from losses comes down mostly to:

- The types of loans you lend in.

- The ability of P2P lending sites to assess the risk of incurring losses on a loan, and to set a sensible interest rate or reject the application accordingly.

- The steps you take to spread your money across a large number of loans and P2P lending sites.

And that is just as well

Reserve funds are not usually so full of cash that they will completely protect you in a severe recession or property crash, and that is not their job.

If you were completely protected from all risk, lenders would pile in so much cash that it would push interest rates right down. If that happened, they might even go so low that you could barely tell the difference between savings accounts and peer-to-peer lending.

There has to be a noticeable element of short-term risk for lenders to demand, and get, higher rates than those paid by Barclays Bank.

The limitation of reserve funds

I know I’m sort of repeating myself, but reserve funds are not supposed to protect you completely from losing any money on every single loan you lend in. They are there to protect you from initial or forecast losses.

In the case of RateSetter, the CEO has specifically stated that its reserve fund is not designed to withstand a 1-in-100 year recession.

Update on 9th July 2020: RateSetter and the others mentioned below have now proven my point, eight years after the first reserve fund was created – by RateSetter. RateSetter and Lending Works have had to divert additional lender interest to their reserve funds to protect lenders. Growth Street has pooled loans so that interest can make up the shortfall in the reserve fund.

Lending Works*, which has a fat reserve fund, can withstand considerably more bad debts than it is getting now. But its own pot too would likely be overwhelmed in such a poor economic environment.

Growth Street (now closed to lending as of 9th July 2020) has (had) a reserve fund that is very large indeed compared to the overall loan book, its recovery rates are better than many other P2P lending sites with reserve funds and, I think, it would likely inject more cash into the fund if necessary. Yet over the past few months it has built up a number of borrowers with massive loans in it that could overwhelm the pot.

Reserve funds are just icing on a cake

If your heart is pounding on reading the above, never fear. Just don’t miss the main point: the good news is that P2P lending sites offer other stronger defences against losses.

Some of these reserve funds will at times be busted and need to be rebuilt, but that’s all part of the plan these and other P2P lending sites have.

Each of the three reserve funds I’ve mentioned are about 2%-4% of the total amount of loans that they are protecting. However, the interest lenders are earning is typically 5% to 7%.

And that interest is not one-off, but per year, which increases its worth.

At Lending Works, for example, if you don’t choose to re-lend the monthly repayments from your borrowers, the interest you earn over several years would boost the total interest earned on its longer-term lending account to closer to 9% or 10%, provided you don’t sell out early.

If you re-lend every month, the total interest you earn, before losses will be much higher still.

So the interest you earn offers far greater protection against losses, as it is of far greater size than the reserve funds.

Even so, with a reserve fund gone, you could suffer from bad luck compared to the average lender, so here are…

Three ways to get completely prepared for reserve fund failure

You have three very simple things to do to be prepared for reserve funds getting depleted:

- Go with the flow. Accept that some reserve funds can and will be wiped out at times and don’t let it bother you when it does. If you’re not comfortable with that, you probably shouldn’t be lending your money, because, when you react in panic, it is likely to mean you sell your loans before you’ve earned enough interest to cover any losses.

- Spread your money across lots of loans and P2P lending sites, so that you can’t easily suffer from bad luck or from poor lending decisions.

- When looking for P2P lending sites with reserve funds, look for the ones that share the risks between all lenders by pooling loans when bad debts rise a lot. The three P2P lending sites mentioned above all do this, in different ways. Basically, if the money in a reserve fund gets too low or wiped out, all lenders will equally share the cost of any further losses, as if they were all lending across all the outstanding loans, rather than a small batch of them.

Read more:

Is Peer-to-Peer Lending Safe For Lenders?

The 13 Key Peer-To-Peer Lending Risks Risks.

3 Huge P2P Lending Mistakes You’re Making Now.

Visit Growth Street, Lending Works* and RateSetter*.

Independent opinion: 4thWay will help you to identify your options and narrow down your choices. We suggest what you could do, but we won't tell you what to do or where to lend; the decision is yours. We are responsible for the accuracy and quality of the information we provide, but not for any decision you make based on it. The material is for general information and education purposes only.

We are not financial, legal or tax advisors, which means that we don't offer advice or recommendations based on your circumstances and goals.

The opinions expressed are those of the author(s) and not held by 4thWay. 4thWay is not regulated by ESMA or the FCA. All the specialists and researchers who conduct research and write articles for 4thWay are subject to 4thWay's Editorial Code of Practice. For more, please see 4thWay's terms and conditions.

*Commission, fees and impartial research: our service is free to you. 4thWay shows dozens of P2P lending accounts in our accurate comparison tables and we add new ones as they make it through our listing process. We receive compensation from Lending Works and RateSetter, and other P2P lending companies not mentioned above either when you click through from our website and open accounts with them, or when you make an investment, or to cover the costs of conducting our calculated stress tests and ratings assessments. We vigorously ensure that this doesn't affect our editorial independence. Read How we earn money fairly with your help.

To get the best lending results, compare all P2P lending and IFISA providers that have gone through 4thWay’s rigorous assessments.