See why 4thWay now accepts ethical ads.

See why 4thWay now accepts ethical ads.

CapitalStackers Update On COVID-19 25th March, 2020

By CapitalStackers.

Financial hygiene is even more important during the COVID-19 crisis

Total transparency has always been a core function to us at CapitalStackers*, but in the current climate, just like handwashing, this element of normal housekeeping takes on critical importance.

We’re fully aware that our investors will be looking to us to keep them informed as the COVID-19 crisis unfolds. Of course, detailed information has always been available in the individual deal rooms on the platform. But for those investors who may not go looking for this, there’s a chance they could miss important information.

So to be clear, we’ll be reporting even more regularly to you – both in general terms, and on a deal-by-deal basis. We’ll give you all possible detail on how conditions on the ground are affecting the specific projects that you’ve invested in.

Clearly, we can’t predict how things will pan out, but by continuing to give you regular, exhaustive progress reports on each project – both from the borrower, and from the independent surveyor – we hope to give you all the information you need to assess the ongoing safety of your investments.

If you’re investing through a pooled platform – across a variety of consumer and SME loans – your capital is more likely be affected in the immediate to short-term. If you’re able to, you might want to withdraw your funds quickly because the situation is volatile and information hard to come by, but this may no longer be possible.

On the other hand, when you lend direct on a property development scheme through CapitalStackers, the situation is going to be played out over a longer term (excepting projects where completion is imminent), so the need to move quickly is not quite so crucial.

Of course, you’ll want to keep a closer eye on the situation – but you’ll also have an ongoing, detailed rundown of every key element of the investment. As we say, this is available on the platform at all times, but over the coming months we’ll go further and interpret it more frequently so that you don’t miss a thing.

And while the current situation could never have been foreseen, our standard due diligence builds in some fairly significant downsides for every scheme because we have always felt it prudent to do so. This, therefore, leaves you a fair amount of headroom before the virus infects your capital.

For instance, if we’re (collectively) lending within our typical range up to a maximum 75% loan-to-value including interest, this means the sale price will have to fall by more than 25% from the appraised valuation before your capital is affected. However – this is also after we’ve allowed for potential construction delays, cost overruns and deferred sales.

That’s quite a lot of breathing time.

Then again, we’re not rejecting the possibility that property values could be hit hard in the coming months, but as you’d expect, we’ve considered this in our risk analysis too.

And without doubt, the most important thing you want to know right now is how all this could impact our deals, and your investments. We’re going to try to answer this question here, but please be aware that the answer will extend and adapt as the situation does.

What could the effects be?

This is new territory for everyone. The whole world has changed and seemingly changes again every time the sun comes up. Accurate prediction is nigh on impossible but here are our best conjectures about the immediate impact:

Project periods may need to be extended because:

- Skilled labour supply might be reduced.

- The supply chain could be interrupted.

- Utility companies may decrease output or even go into self-imposed lockdown.

- A blanket lock down on all sites could be imposed by the Government if on-site working practices on some sites fail to adhere to safe distancing rules.

- Projects nearing completion will certainly be impacted by the current general lockdown. If people can’t view, they won’t be able to buy and so selling periods will become protracted.

We can expect longer construction periods to lead to increased costs and higher interest accrued through longer-than-anticipated loan terms.

In addition to the above, property values may fall due to a weaker economy.

These factors will eat into the profit margin and push up the loan-to-value ratio.

So what are we doing about it?

In short, we’re going through our daily downside sensitivity routine, but on steroids. We’re appraising each deal in the context of where it is now, assessing the possibility of a total construction lockdown, evaluating delays to construction and sales with interest continuing to roll up.

Through this exercise, we’re able to give you a progressive insight into how much values could fall before you are on risk.

Although the situation is unprecedented, we’re also able to draw from historical examples in our modelling, and this gives us some cause for optimism.

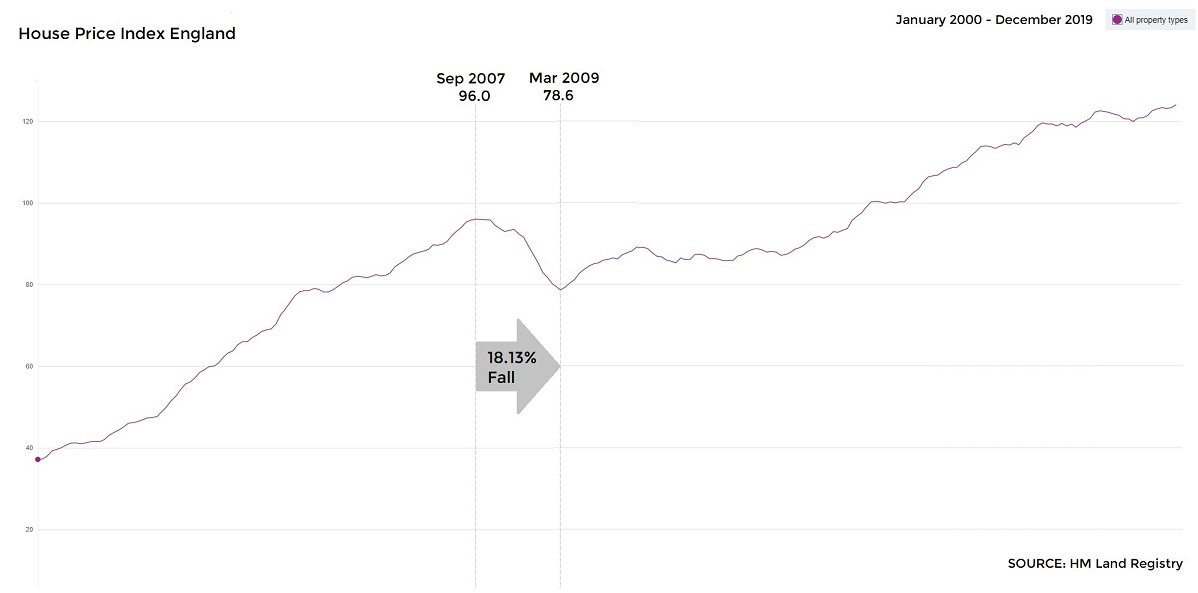

The last massive interruption to the market came in 2008 when the banking sector imploded and liquidity almost completely dried up. As you can see from the chart below, the market fell less than 20% in the eighteen months from the peak in September 2007 to the trough of March 2009. This, of course, is less than the minimum 25% headroom all CapitalStackers deals allow for.

The banking sector at that time was less robust than it is now. Some banks collapsed, others simply pulled out – leaving the property sector in the lurch. It took a long time for the market to get back to where it was.

Today, banks have better capital ratios and their real estate exposure is significantly more conservative. The expectation and likelihood is that they will remain supportive while the market repairs itself, and that the repair should be quicker and more stable than last time.

So to summarise, as always, we’re maintaining close contact with our borrowers, senior debt providers, monitoring surveyors and estate agents – but everyone is on high alert and we’re fully aware of the increased importance of full and detailed information.

And as ever, we’re making ourselves fully available to investors. You’re used to that, of course, but now, more than ever, if you want to discuss the outlook either generally or specific to any deal, you’re welcome to call us at any time.

Read the CapitalStackers Review.

To get the best lending results, compare all P2P lending and IFISA providers that have gone through 4thWay’s rigorous assessments.