See why 4thWay now accepts ethical ads.

See why 4thWay now accepts ethical ads.

Peer-to-Peer Lending Vs Bonds

Most peer-to-peer lending sits in the sweet spot with potential rewards considerably above savings accounts and yet risks below the stock market.

Most peer-to-peer lending sits in the sweet spot with potential rewards considerably above savings accounts and yet risks below the stock market.

And its incredibly steady record since 2005 certainly supports that.

But where exactly does peer-to-peer lending sit compared to bonds?

Peer-to-peer lending has a huge number of advantages over bonds.

That’s why I seriously got into P2P lending in the first place, and helped found this website in 2014. And, while I continue to invest extensively in shares, I’ve never wanted to invest in a bond in my life.

So, let’s take a look at the general differences between P2P lending and bonds. Then we’ll look at differences with some specific types of bonds.

Who you lend to

Depending on your risk appetite and diversification strategy, peer-to-peer lending usually involves lending to creditworthy small-and-medium sized businesses, individual borrowers, those who rent out commercial properties, or lending to landlords.

Going up the risk scale, it cam mean lending to fund property developments, lending against properties that are currently untenanted, or lending to people currently low on cash but who have luxury assets, such as yachts and artwork. It can even mean lending to individuals or businesses that are barely creditworthy for higher interest rates.

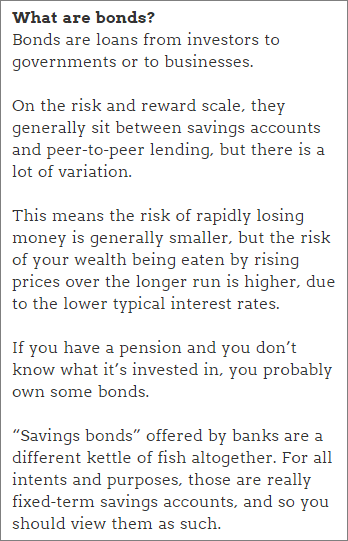

Bonds are usually loans to creditworthy large businesses or to governments.

Security

Both peer-to-peer lending and bonds is a real mixed bag when it comes to what property can be repossessed and sold to recover your money if the borrower fails to repay.

In both cases, the loan might be secured or not. However, a great deal of secured P2P lending is against real property (real estate). The borrower can’t sell up or borrow more money against the property without the lenders’ permission.

In contrast, the security on bonds is generally less tangible. Specifically, the borrower can often use up the security before it goes under. For example, that might mean wear-and-tear on machinery used as security or burning through cash reserves.

Not all P2P lending or bonds are secured at all.

Bad-debt provision funds and other enhancements

Bonds and bond funds don’t have a pot of money set aside to pay expected bad debts. Some P2P lending websites do.

Reserve funds aren’t always suitable for lenders, but sometimes they are fantastic “credit enhancements” and it’s great to have the choice.

In addition, peer-to-peer lending has some quite interesting additional protections. For example, directors or providers sometimes take the first loss.

Transparency

Bonds and bond funds do not have the level of transparency that the peer-to-peer lending industry is leaping towards.

It’s not just public information but what they provide to third parties such as 4thWay. Many peer-to-peer lending websites already send 4thWay their entire loan book details regularly so that we can review and analyse how each of their historical loans has performed. Or they even publish the loan books for all to see.

This is an unprecedented amount of useful information and this huge knowledge advantage lowers the risks for lenders dramatically. Many of the P2P lending companies also allow you to speak directly with the decision makers, so you can size them up for yourselves.

Duration

Bonds last on average around 10 years. The average duration for P2P lending is under three years, which, when combined with good interest rates, is an attractive quality for many investors.

Loan payment schedule

Bonds are invariably interest-only loans, with the initial loan repaid at the end in one go, or rolled over when the borrower issues a new bond to repay the old one.

Peer-to-peer lending is more diverse. It’s a lot of interest-only lending and sometimes its “full bullet”, which means not just the loan but also all the interest is paid at the end. This variety means you can lend to more different types of borrowers with different needs.

When you’re lending for longer than three years, peer-to-peer lending is often repayment lending. This means that every month the borrower repays not just some interest, but also some of the initial loan.

Repayment loans have some interesting characteristics:

- If the borrower suddenly can’t pay half way through, at least you have already received a good portion of your loan back already.

- You get a better record of repayments and you get it earlier on, so you can see better how borrowers are likely to do.

- It’s easier for borrowers to budget for repayment lending and there’s no need to worry about whether the planned exit strategy will fall apart years into the debt.

- You can begin re-lending your money at higher rates quickly if interest rates are rising.

Lending direct versus funds

Peer-to-peer lending involves lending directly to a borrower and then waiting until the borrower has fully repaid the entire loan and interest naturally.

Many P2P lending websites make it easy for you to lend to dozens or hundreds of borrowers in precisely that way, but without the extra costs of lending through an investment fund.

Bond lending, on the other hand, is usually done through investment funds.

Investment funds change the game of investing somewhat, because the bond fund manager buys – and sells – bonds for you at different stages in the life of the loans – and at different prices, depending on what the other investors in the market believe.

The result of doing so is that the investments become much more volatile. The fund might at times buy bonds for considerably more than they were issued for (perhaps taking a bet that someone will buy it for even more later).

In other words, the initial bond buyer might have lent £1 million, but your bond fund manager might pay £1.1 million from your fund’s pot to take on those loans. On the flipside, this also gives you the opportunity of making a profit by selling higher.

Early exit versus stable interest rates and results

P2P lending is more focused on stable interest rates than on being certain you can get your money back before the borrower repays you naturally. The lending rates are usually set by professionals and, after that, rates are not usually influenced substantially by what investors think. You might sometimes be tied in longer than you wanted, but you generally expect to keep earning steady interest while you wait to get out.

That’s very to different to investing in bond funds. Bond funds prioritise being able to sell up whenever you want over stability of your returns, which can fluctuate a lot more with supply and demand.

Most P2P lending websites have secondary markets that allow you to buy and sell loans to other lenders. These have functioned well during good times, allowing lenders to access their money early most of the time. But you should see this more as a bonus than a permanent feature.

When lending money in any way, the natural life of the investments is the time it takes for borrowers to repay their loans and interest. P2P lending often enforces this discipline on you, whereas investors in bond funds often fight the natural life, which comes at the cost of selling at a cut price when you leave.

Reducing the risk of chance

Most bonds and most P2P loans are to solid borrowers, but an advantage in P2P lending is that you can more easily spread across far more loans. Indeed, thousands of them. With little effort. This seriously reduces the risk of losses through bad luck and replaces any potential safety premium you might get when you lend to giants. A lot of the time, that perceived additional safety is not even real, when quality P2P lending matches the risk of corporate borrowers.

Taxes

You have to pay income tax on bonds or bond funds unless they are wrapped up in an ISA or pension, which are low-tax wrappers for your investments.

With most bonds, you do not have to pay capital gains tax if you sell the bond for a profit.

The first £1,000 of interest you earn in a tax year in peer-to-peer lending and savings accounts combined will be tax-free. You might have to pay capital gains tax if you sell your loans to another lender for a profit, although this might only happen if you’re selling a loan part that you bought second hand yourself. In practice, it doesn’t happen often and you are allowed to use your generous personal capital-gains tax allowance.

Some peer-to-peer lending is already available in pensions, but you should expect the costs right now to be prohibitive unless you have a very large amount to lend.

You can also now lend through “Innovative Finance ISAs”, or “IFISAs” for short, which simply allows you to lend tax free. Usually, these come with no, or minimal, extra costs.

Read more on this in How Is Peer-to-Peer Lending Taxed?

Compared to government bonds

Now let’s look at a few different types of bonds, starting with government bonds.

While governments do from time to time go bankrupt and end up paying back less than they owe, lending to governments is generally safer than lending to companies or individuals.

Although it does depend on what your definition of safe is.

The interest rates you earn on government bonds is generally so low that people lending to governments can actually be confident of being less wealthy as the years go by.

That’s because you should expect the prices of goods and services to rise so fast that the meagre interest you earn in government bonds won’t even cover that extra cost during your weekly food shop.

So it’s very like saving with savings accounts in that way: a safe way to steadily watch your wealth dwindle.

Compared to corporate bonds

When most people talk about lending to businesses, I think they’re generally referring to corporate bonds.

Corporate bonds make up the majority of bonds to businesses. They’re almost invariably to large or very large businesses.

These loans are normally pretty safe and so interest rates are often not much more than government bonds.

So you have the same problem that “too safe” also means too low returns to beat rising prices, especially after the costs of lending.

If you lend through a bond fund, you can get the additional price-fluctuation risk mentioned earlier.

Compared to high-yield bonds

The contrast between high-yield bonds and peer-to-peer lending is probably the most interesting one.

These bonds pay more interest (a higher “yield”) than corporate bonds and are also noticeably higher risk. While you’re still generally lending to large businesses, you’re looking at businesses that are not as sound.

While interest rates can be similar to peer-to-peer lending, P2P is generally lending to the best borrowers, be they companies or individuals, with the main difference being that they are smaller, and the loans are smaller.

Compared to retail bonds

Retail bonds are corporate bonds that are generally sold directly to individual lenders, rather than bought up by investment funds.

These are still normally loans of more than £100 million – far larger than P2P – and to medium-or large sized businesses.

Retail bonds are sold individually and are not usually vetted by an intermediary such as a peer-to-peer lending website.

It’s also harder to get out of a retail bond early than it is to get out of larger bonds. It pays to be wary of retail bonds.

Compared to mini-bonds

But not as much as you need to be wary about mini-bonds.

Mini-bonds are like a light version of retail bonds in that you get far less information from the business borrower and even less outside scrutiny. These are still typically large loans, at over £50 million.

The plus sides for the business borrower is that it’s probably quicker, easier and cheaper to issue mini-bonds. Another potential plus for some businesses is that they might find it easier to hide their skeletons in the closet.

Compared to savings bonds

Savings bonds are, for all intents and purposes, savings accounts. They are offered by banks and building societies and you see them every time you compare savings accounts online. You can get them wrapped in cash ISAs. These usually pay a fixed interest rate, and they last for six months to five years.

Further reading

“Even if you could invest in bonds at no cost, the best historical records show that you could have invested regularly, month after month, with disappointing results. You could still very easily have found, after 20, 30 or more years, that your investments can buy you less in the shops than when you put the money in.”

Read more in Peer-to-Peer Lending Vs Other Investments.

And more!

The Investment That’s Better Than Peer-To-Peer Lending.

The Right Split Between Savings, P2P, Shares, Property.

Why Does P2P Lending Pay Investors Higher Rates Than Bonds?

Peer-to-Peer Lending is Better Than Bonds.

To get the best lending results, compare all P2P lending and IFISA providers that have gone through 4thWay’s rigorous assessments.

Independent opinion: 4thWay will help you to identify your options and narrow down your choices. We suggest what you could do, but we won't tell you what to do or where to lend; the decision is yours. We are responsible for the accuracy and quality of the information we provide, but not for any decision you make based on it. The material is for general information and education purposes only.

We are not financial, legal or tax advisors, which means that we don't offer advice or recommendations based on your circumstances and goals.

The opinions expressed are those of the author(s) and not held by 4thWay. 4thWay is not regulated by ESMA or the FCA. All the specialists and researchers who conduct research and write articles for 4thWay are subject to 4thWay's Editorial Code of Practice. For more, please see 4thWay's terms and conditions.