See why 4thWay now accepts ethical ads.

See why 4thWay now accepts ethical ads.

Is P2P Lending Going To Be Rocked Like Private Credit?

A number of funds that mimic the role of banks have sustained losses. Furthermore, they’ve had to restrict withdrawals from investors, sparking concerns of weaknesses in the global financial system.

You might have read about these problems repeatedly over the past half year. It’s called “private credit”.

There hasn’t been a snowball of collapsed lending or anything like that. But a few big names with private-credit funds in the US have caused concern.

One of the biggest is fund manager BlackRock. Earlier this year it marked down 19% of its private-credit fund’s assets1.

That’s a huge write-off when you consider that money lending, generally speaking, is supposed to be substantially more stable than the stock market.

So I’m writing today about the differences and similarities in risks within private credit versus P2P and other online direct lending.

Hypermassive growth precedes doom

Sarah Breeden, deputy governor of the Bank of England, said recently that the enormous growth in the private credit “shadow banking” system has not been tested.

She told the BBC: “Private credit has gone from nothing to two-and-a-half trillion dollars in the last 15 to 20 years. It hasn’t been tested at this scale with the degree of complexity and interconnections it has with the rest of the financial system so far.”2

While the private credit issues have been mostly in the US, there are parallels in the UK’s trajectory. Because it starts with hypermassive growth.

UK Finance found that private credit grew at a compound rate of 43% per year since 2013 to hit £59.5 billion in 2024. So basically £60 billion.

In the UK, £60 billion of private credit just replaces a little over 10% of similar bank lending. But it’s still an extraordinary growth rate to sustain for more than a decade.

As Moody’s said: “Historically, rapid loan growth…has preceded asset-quality deterioration. Weakening asset quality often follows looser underwriting and aggressive lending strategies, the negative effects of which may only become apparent years later and typically during economic downturns.“3

Here, the contrast with P2P lending is huge.

The P2P lending market’s growth over the same period has been impressive, but still far more sedate.

I’ve just done a back-of-the-envelope calculation, but it comes to around 12.5% growth per year. So this market still remains surprisingly small when you look at P2P lending’s long-term results for lenders and borrowers alike.

But the concerns with private credit are not just about its growth rate.

People are also worried about potential investing losses and about their money getting tied in. Let’s split those two categories up further to see the similarities and differences with P2P lending.

The risk of losses in private credit is totally different to P2P lending

A lot of private credit comes from banks doing “originate to distribute”. It works as follows:

- A lender – typically a bank – assesses loan applications, approves the loans at specific rates and terms, and issues the funding.

- It then bundles lots of similar loans together, repackages them, and sells them to investors who buy units in a private-credit fund.

If that sounds disturbingly familiar, it should.

It was similarly repackaged debt that greatly contributed to the Financial Crisis of 2008. These collateralised debt obligations – CDOs – were nicknamed “weapons of mass destruction”.

The repackaging makes it much harder for investors to understand the risks in what they’re buying. These sorts of chains can remove banks from caring about the risk, as they can pass the buck.

That’s what happened in the lead-up to the Financial Crisis. Banks made their large fees from the repackaged debt sales and wiped their hands of it.

If the 2008 disaster and Breeden’s words are anything to go by, we can also presume that investors and fund managers are not getting sufficient details about the risks in the repackaged debt.

It’s the concoction of opacity and the lack of skin in the game after the loans are out of their hands.

Contrast that with P2P lending and other online direct lending:

- The P2P lending providers haven’t raised the debt, repackaged it and sold it on to some fund manager for their investors to buy units in. Instead, it has offered the loans to individual lenders to fund directly.

- The level of transparency (generally speaking) in the P2P market is huge on such things as loan performance and the characteristics of each loan. The loans are clear to see. Arguably even more so than the bond debt market.

- P2P lending companies earn their money through the life of the loans (and often even sacrifice their cut if a borrower can’t repay in full). They don’t merely sell the loans and move on.

- It’s the P2P providers’ reputations that are at stake if it doesn’t work out well for lenders. Contrast that with Blackrock’s 19% write-down: I can’t even recall reading which banks were actually responsible for that!

In short, banks bundle together and sell on to others the loans that they’re unwilling or unable to do for regulatory reasons. Potentially packaging them in a way that can’t be understood.

P2P lending is almost always direct, standard, bread-and-butter lending. And typically (although certainly not always) it’s done in a reasonably, or even highly, transparent way.

It’s the opacity of private credit that is giving central banks cause for concern.

Private credit is unsecured lending, while most P2P lending is secured against property

Private credit is mostly unsecured business lending to medium-sized businesses.

There’s a bit of unsecured P2P business lending – mostly to small businesses.

However, the vast majority of P2P lending is lending to property owners. The P2P loans are secured against properties, usually with a legal charge much like you have if you own your own home with a mortgage.

Valuing properties is much easier than valuing medium-sized businesses.

And recovering bad debt is much easier if you can simply get a property sold than if you’re hoping that a bankrupt business still has enough cash and other equipment of value left to repay most of your debt after it’s burnt through everything in a hopeless attempt to keep going.

Your money sometimes gets trapped in

Even so, lenders in P2P can still learn an important lesson from this private credit story.

Investors in private credit funds operated by giants like BlackRock and Blue Owl Capital were spooked by high-profile defaults, so many investors tried to pull their money out at the same time.

The numbers were large enough that those funds had to limit withdrawals, as per their terms and conditions.

Here, P2P lending is exactly the same – and yet it’s by design.

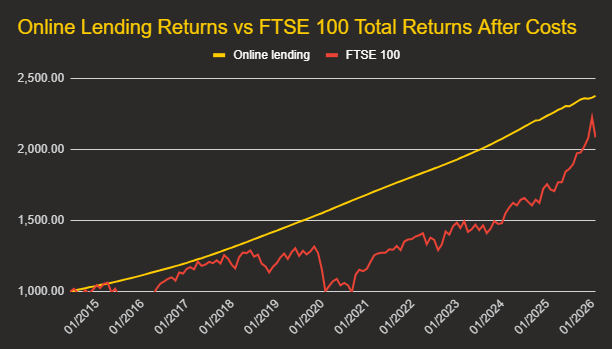

With P2P, you get stability of returns that share investors would be extremely envious of:

While steadily earning interest in most loans, it’s normal for people to become uncertain and want to pull money out.

Being “spooked” is something that can happen to lenders regardless of how well things are going.

It’s not just that your money getting tied in can happen – it does happen, it has happened and will happen.

That’s even when you lend in excellent loans through lending accounts that normally allow you to exit early.

P2P lending is usually a stable type of investment but as a direct consequence of that stability it’s an “illiquid” investment.

“Illiquid” means that you can’t expect to always be able to get out of the loans before borrowers actually repay them. You’re tied in until the money is naturally repaid.

Indeed, I loved the title to some recent CEPS research by Apostolos Thomadakis on private credit: “Private credit’s problem isn’t illiquidity – it’s the illusion of liquidity”4.

The whole point being that this is a trade-off that lenders are supposed to understand. Thomodakis makes the same points 4thWay has repeatedly made about P2P!

Pages linked to above

4thWay P2P And Direct Lending Index: Q1 2026.

To get the best lending results, compare all P2P lending and IFISA providers that have gone through 4thWay’s rigorous assessments.

Sources:

1. Private Debt Investor: BlackRock BDC Marks Down NAV By 19%.

2. BBC: Stock Markets Are Too High And Set To Fall, Says Bank Of England Deputy.

3. Moody’s: US Banks’ Private Credit Loan Exposure Nears $300 Billion.

4. Download the research CEPS: Private Credit’s Problem Isn’t Illiquidity – It’s The Illusion Of Liquidity from here.

Independent opinion: 4thWay will help you to identify your options and narrow down your choices. We suggest what you could do, but we won't tell you what to do or where to lend; the decision is yours. We are responsible for the accuracy and quality of the information we provide, but not for any decision you make based on it. The material is for general information and education purposes only.

We are not financial, legal or tax advisors, which means that we don't offer advice or recommendations based on your circumstances and goals.

The opinions expressed are those of the author(s) and not held by 4thWay. 4thWay is not regulated by ESMA or the FCA. All the specialists and researchers who conduct research and write articles for 4thWay are subject to 4thWay's Editorial Code of Practice. For more, please see 4thWay's terms and conditions.